8x EV/Earnings and a SaaS For Free

8.2x EV/Earnings.

29% operating margins.

Emerging segment growing 70%, with an embedded SaaS for free.

Debt-free, with net cash ~24% of market cap.

Buying back shares, ~8% of shares retired in 2.5 years.

Loss-making subsidiary dissolved.

Potential NASDAQ uplisting.

For the first few years of investing, my framework was built around the compounding style of Phil Fisher and Nick Sleep. Wonderful businesses, strong moats, and long runways of growth. These were mostly large and mega caps, with the occasional small cap.

But at some point, I started asking whether I was playing the right game. Because there’s a ceiling to what that approach can realistically deliver.

A trillion-dollar company can double, but the forces required to move that needle are tremendous. Doubling a $100 million market cap stock is a much shorter journey.

That’s why I started looking at microcaps, and quickly realized that market inefficiencies are real. And there’s a structural reason for that: institutional money simply can’t get in. The funds are too big and the positions too illiquid.

For a retail investor with small amounts of capital, that structural gap is where the edge lives.

When you find the right situation, you can significantly stack the odds in your favor. The upside can be high, with limited downside, if you have a margin of safety underneath.

That’s also why casinos don’t interest me anymore.

Why take a 48% bet in a roulette game when you can find a stock with much higher odds in your favor? Plus, if the roulette bet goes wrong, you lose everything. But lose on a stock with a margin of safety, and you walk away with most of your chips still on the table.

This is one of those bets.

Currency Exchange International Corp (CURN: OTC) (TSX: CXI)

Business Overview

Currency Exchange International (CXI) operates two core segments:

Banknotes (~83% of total revenue in 2025) provides physical foreign currency exchange such as buying and selling banknotes to banks, financial institutions and retail customers.

Payments (~17% of total revenue in 2025) handles international and domestic wire transfers and foreign check clearing for banks and financial institutions.

The banknotes segment breaks down into:

Wholesale (~42% of banknotes revenue in 2025) supplies foreign currency directly to financial institutions and money service businesses.

Direct-to-Consumer (DTC) (~41% of banknotes revenue in 2025) serves retail customers through company-owned branches, agent locations including AAA travel clubs and airport operators, and OnlineFX, a proprietary home delivery platform.

The wholesale model is straightforward. When a community bank needs foreign currency, they order from CXI. CXI ships the banknotes via third-party armored carriers and insured couriers.

When I first came across this stock, I thought it was a declining business in a sunset industry since it’s essentially just supplying cash. And isn’t the use of physical cash dying?

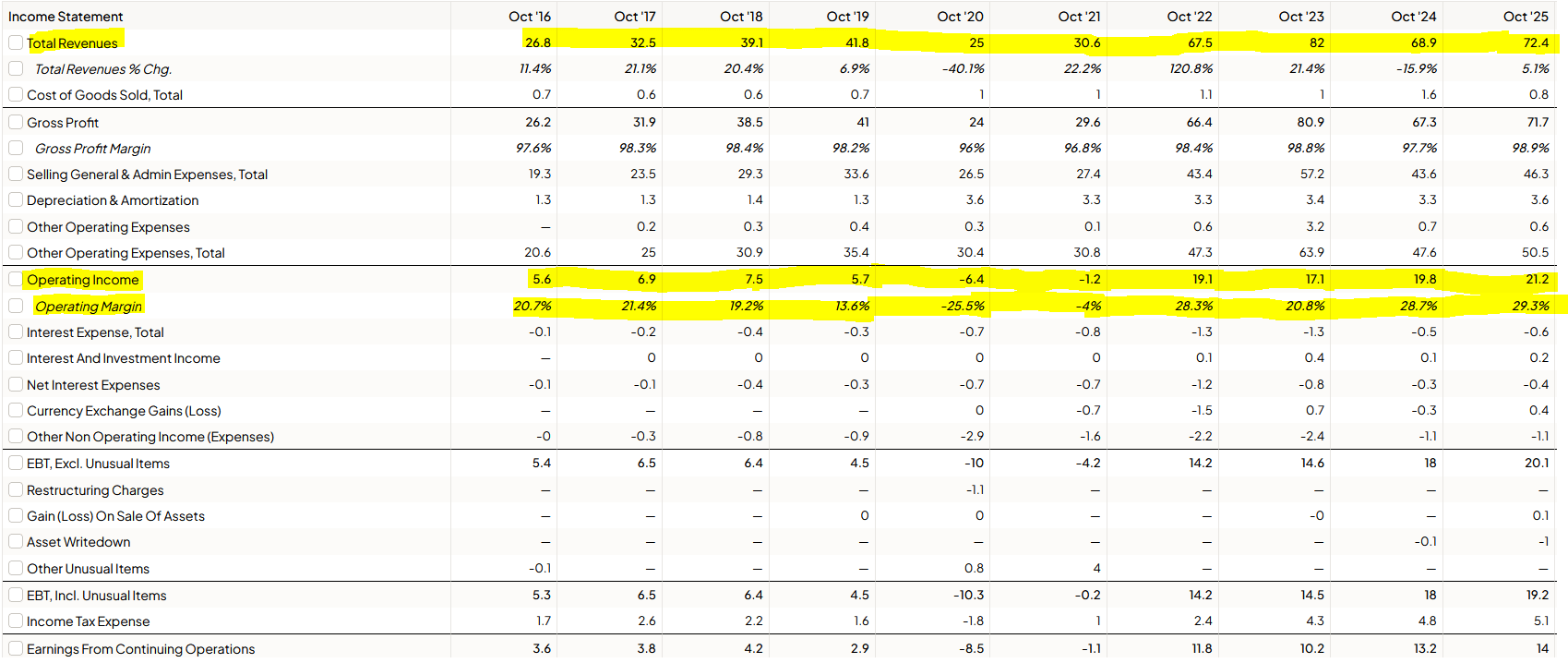

Here’s a look at CXI’s financial performance for the past 10 years:

Revenue has grown at a CAGR of 10.6% for the past 10 years.

Revenue declined 40.1% in 2020 due to COVID, but rebounded strongly with a 23.7% CAGR from 2020-2025, driven by the COVID recovery period and market share gains from Travelex, CXI’s biggest competitor, who went bankrupt in the same year.

Operating profit was positive every year except 2020 and 2021, when COVID travel restrictions hit hard.

Free cash flow has been positive every year except 2020 and 2023.

At first glance, CXI’s free cash flow looks lumpy and volatile. But there’s some nuance here.

The negative free cash flow in 2020 was one-off due to COVID. The lumpiness in other years, including 2023, comes down to working capital timing. Let me explain.

CXI moves billions in currency annually. When a bank orders a shipment, CXI delivers first and collects payment within 24-48 hours. But CXI's financial year ends October 31st, and some trades will be mid-settlement at year end based on order timing.

When receivables are unusually high and payables unusually low, cash flow gets distorted. In 2023, receivables increased by $6.9 million (meaning CXI was awaiting payment) and payables decreased by $10.7 million (meaning CXI had already paid counterparties). That’s $17.6 million distorting free cash flow in a single year.

Zoom out over 10 years and the picture is cleaner. CXI averaged $8.6 million in free cash flow per year, with a free cash flow yield of 8.6% and that’s including the COVID year. Excluding 2020, average free cash flow rises to $9.7 million per year, with a yield of 9.8%.

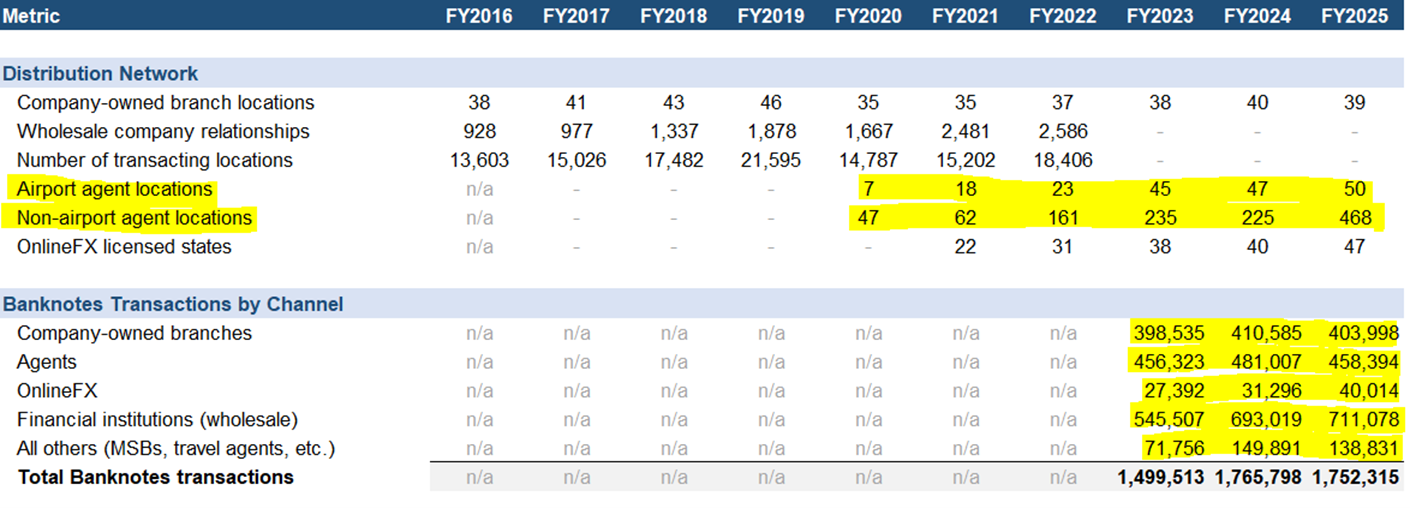

The operational picture over the same period:

2019 marked the peak, with 46 company-owned branches and 21,595 transacting locations before COVID.

In 2020, CXI pivoted toward an asset-light, agent-driven distribution model. Airport agent locations grew from 7 to 50 between 2020 and 2025, while non-airport agent locations expanded from 47 to 468. Company-owned branches held steady in the 35-40 range.

Banknote transactions grew 17.8% in 2024, and were broadly stable in 2025 with a slight decline of 0.8%.

Banknotes isn’t a dying business. It’s still growing, just slowly.

The COVID recovery and Travelex market share gains drove a 23.7% revenue CAGR from 2020-2025. Strip those out and the core business looks slow and steady.

That’s not a bad foundation. Stable revenue, 20%+ operating margins, and healthy free cash flow yield.

But that’s not why I’m writing about this stock.

Which brings me to Payments.

Payments: The Emerging Segment

For the past 10 years, CXI operated in both the US and Canada. The US directly through CXI, and Canada through its wholly-owned subsidiary Exchange Bank of Canada (EBC).

CXI established EBC in 2016 as a wholly-owned, federally chartered Canadian Schedule I bank, initially to distribute physical US dollar banknotes internationally and provide foreign exchange payment services to Canadian businesses.

It was basically an expansion into the Canadian market.

But for most of its existence, EBC was a financial drag.

EBC’s corporate payments business faced margin compression and customer attrition in an increasingly competitive environment, while its international banknotes business stalled because EBC’s balance sheet was too small to provide the credit comfort global counterparties required, particularly after US regional bank failures in 2023 caused credit departments worldwide to tighten requirements. The regulatory and compliance overhead for operating a standalone Canadian bank was too high relative to the revenue it generated.

EBC lost $10.7 million in 2024 and $3.7 million in 2025. Prior to that, losses were buried inside the consolidated numbers and never broken out separately.

After years of losses, CXI finally pulled the plug on Canada in February 2025. Operations ceased in October 2025, and the bank was formally dissolved in April 2026, with remaining net assets repatriated to CXI.

US Payments

Meanwhile, the US tells a different story.

Canada’s banking industry is dominated by the “Big Six” banks, which control over 90% of total banking assets.

In contrast, the US is far more fragmented. The “Big Four” banks hold just ~50% of total banking assets, with the remaining half spread across more than 4,000 community banks and financial institutions.

CXI's strategy was to integrate directly via API into the core banking software that thousands of US community banks already run on, starting with Fiserv's WireXchange in 2019, followed by Jack Henry's SilverLake in 2021, and eventually Finastra and several others.

These API integrations meant a bank’s existing software could plug straight into CXI’s payments and FX infrastructure without ever switching systems.

US payments grew at a respectable but unspectacular 19-32% annually through 2025, never really moving the needle on the overall business.

Then something changed.

The Hidden SaaS

In the US, when a bank initiates a domestic wire transfer, they do it directly through the Federal Reserve through FedLine. FedLine is the Fed’s proprietary network that allows financial institutions to submit payment instructions directly to the Fed for settlement.

When initiating an international wire transfer, banks use SWIFT, a global messaging network that transmits payment instructions between banks across different countries.

But most community banks don’t have their own FedLine or SWIFT access because it requires technical setup, ongoing compliance obligations, and dedicated staff to manage. It’s basically not worth the resources for a small bank doing modest wire volumes.

Instead, they typically route both domestic and international wire transfers through correspondent banking relationships with larger banks such as JPMorgan, who have their own FedLine and SWIFT access, acting as the middleman and charging per-transaction fees.

But CXI doesn’t do modest wire volumes. They need to route wire transfers between financial institutions as part of their business.

They route billions in wire transfers.

Which brings us to WireHub.

WireHub was launched in late 2023. It’s a software platform that enables small community banks to route domestic US wire transfers directly through the Fed, bypassing the correspondent banking relationships most community banks rely on.

This is possible because CXI has direct FedLine access. They’re essentially letting banks use their connection with the Fed, by charging a recurring software fee.

Importantly, CXI never touches the money and bears no FX risk.

WireHub had about three banks onboarded for nearly two years.

In the second quarter of 2026, CXI announced that WireHub onboarded 20 banks. And that it’s now fully a SWIFT member.

CXI is also investing to add FedNow to WireHub. FedNow is an instant payment rail that settles 24/7 in real time, designed to eventually replace or complement traditional wire transfers for smaller instant payments.

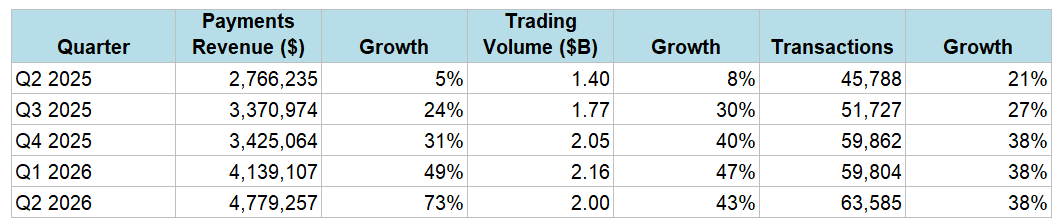

Here’s how US payments have trended in recent quarters (Q2 2025 was the first quarter CXI reported US payments separately):

Payments revenue has been accelerating for the past five quarters, from 5% growth in Q2 2025, to 73% in Q2 2026.

From Q2 to Q4 2025, payments as a percentage of total revenue averaged 16-17%. In Q1 and Q2 2026, that figure increased to 27%.

That’s a fast-growing, high-margin SaaS business that’s largely unnoticed by the market.

Maybe it was the multiple API integrations with the banking operating software that laid the foundation for distribution.

Maybe it was the winding down of EBC that freed up resources to focus on US payments.

Or maybe it’s because community banks are conservative and slow adopters.

The answer is probably a mix of all three.

Market Opportunity

How much can the payments business grow?

The addressable pool is over 4,000 community banks and financial institutions, accounting for roughly half of all US banking assets.

On the Q2 2026 earnings call, CFO Gerhard Barnard laid out the numbers:

Domestic TAM (Total Addressable Market) of ~$450 million.

SAM (Serviceable Addressable Market) of ~$230 million.

SOM (Serviceable Obtainable Market) of ~$120 million.

Payments revenue over the trailing four quarters totals ~$15.7 million. Against a SOM of $120 million, that’s roughly a 13% market penetration of what management views as realistically obtainable.

Capital Allocation

CXI is run by a founder-CEO, Randolph Pinna, who holds 1,408,846 shares (~24% of the company), which is approximately $30 million of skin in the game.

On M&A, management has been disciplined. Over six years of active deal discussions with nothing closed. They continuously identified potential acquisition targets, but walked when the price didn’t make sense.

Instead, the capital has gone into share buybacks and more recently, building out the payments infrastructure. Management remains open to a payments acquisition if the price makes sense.

Here’s the recent buyback history:

Gross repurchases since 2023 total 671,870 shares, or 10.4% of the 2023 share base. Net shares outstanding fell 8.1%, with the difference reflecting new shares issued from stock option exercises over the period.

In November 2025, the board doubled the authorized repurchase program from 5% to 10% of public float.

Pinna confirmed CXI’s stance on the Q4 2025 earnings call:

“Right now the best use of capital is to acquire our stock and retire it.”

Music to my ears.

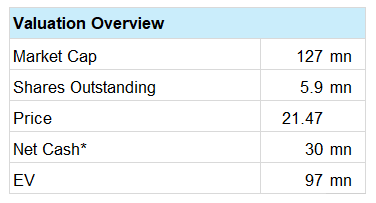

Valuation

A quick note on EV: CXI reports $109.9 million in cash on the balance sheet, but most of that isn't freely deployable. Backing out $57.8 million of banknote inventory, $21.8 million of cash held for customer settlements and other operating requirements leaves $30.3 million in truly free cash, bringing the EV to $97 million.

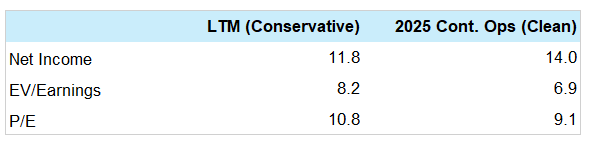

Before putting a multiple on CXI, one question needs answering: what is normalized earnings?

2026 will be the first full clean year with EBC entirely gone.

The LTM figure of $11.8 million is the more conservative one, as it still includes residual EBC operating costs even after stripping out the one-off wind-down charges. The 2025 continuing operations figure of $14 million excludes EBC entirely, giving a cleaner read of the US business alone.

That puts EV/Earnings somewhere in the 6.9-8.2x range.

The reality is likely somewhere in between, and trending higher.

CXI has already generated $4.3 million in adjusted net income in the first half of 2026, before its seasonally stronger second half, which historically accounts for the majority of full-year earnings.

At 8.2x EV/Earnings, you’re paying single-digit multiples for a profitable, debt-free business that’s actively buying back shares.

And you’re getting the payments business, including a fast-growing, high-margin SaaS that has likely hit an inflection point — for free.

Why is it mispriced?

At a sub-$130 million market cap, CXI is small, thinly traded, and below the radar of most institutional investors who have minimum size requirements.

There’s zero sell-side analyst coverage.

Three years of messy financials from the EBC wind-down made normalized earnings almost impossible to read without digging through the filings yourself.

Potential NASDAQ Uplisting

Pinna has flagged a potential NASDAQ uplisting as early as 2027.

University Bancorp, a ~12% shareholder, has advised targeting Russell 2000 inclusion first. The minimum market cap for Russell 2000 entry was $146.4 million as of June 2026. CXI currently sits at ~$127 million.

A NASDAQ uplisting or Russell 2000 inclusion could drive a meaningful re-rating.

Risks

Jack Henry / Fiserv building a competing product: The most obvious competitive threat, but probably the least likely near-term risk. Fiserv generates over $20 billion in annual revenue and Jack Henry over $2 billion. The domestic wire market CXI is targeting is simply too small for either company to prioritize. The more realistic scenario is acquisition rather than competition. That said, CXI adopted a shareholder rights plan in October 2025, which is essentially a poison pill that triggers share dilution against any acquirer who crosses 20% ownership without board approval, making a hostile takeover economically punishing.

Geopolitical and external shocks: Banknotes is a travel and trade-driven business. Wars, pandemics, and political tensions are its biggest disruptors. CXI experienced this firsthand. The demand for the Iraqi Dinar, one of CXI’s top-5 revenue currencies for over a decade, collapsed due to the Middle East conflict. Exotic currencies like the Iraqi Dinar carry significantly higher margins than major currencies, so their disappearance impacts CXI’s margins disproportionately.

Payments and WireHub may not scale: WireHub sat at 3 onboarded banks for nearly two full years before jumping to 20 in Q2 2026. The recent acceleration is encouraging but could plateau again. The good news is that at 8.2x EV/Earnings, you’re not paying for WireHub to succeed. It’s pure optionality.

Acquisition integration risk: Management has $30 million in deployable cash and has been actively pursuing acquisitions for years. A poorly executed deal could disrupt an otherwise clean and growing business.

Wrapping it up

At 8.2x EV/Earnings, you’re getting a founder-led, debt-free business, stable cash flows, and an active buyback program. And on top of that, a payments business with significant runway still ahead.

CXI has shed its loss-making subsidiary, cleaned up its books, and is now emerging with a fast-growing SaaS business that looks like it’s hit an inflection point.

And I don’t think the market has priced any of it in.

DISCLAIMER

This article is for informational purposes only and does NOT constitute financial advice, investment advice, or a recommendation to buy or sell any security. I am NOT a licensed financial advisor, investment advisor, or broker-dealer. The views expressed are my own and based on publicly available information which I believe to be accurate, but I make no representations or warranties as to its completeness or accuracy.

I may hold a position in the securities mentioned. Do your own research before making any investment decisions. Past performance is not indicative of future results. Investing involves risk, including the possible loss of principal.