Datadog: Resilient Growth, Profitability, and a Path to Re-Acceleration

Datadog (DDOG) Q2 2024 Earnings Analysis

1. About Datadog

Datadog is an observability and security software as a service (SaaS) platform for cloud applications that integrates and automates infrastructure monitoring, application performance monitoring, log management, user experience monitoring, cloud security and many other capabilities to provide unified, real-time observability and security for customers’ entire technology stack.

This cloud agnostic and easy to deploy proprietary platform is used by organizations of all sizes and across a wide range of industries. Among some of the use cases include:

to enable digital transformation and cloud migration;

drive collaboration among development, operations, security and business teams;

accelerate time to market for applications;

reduce time to problem resolution;

secure applications and infrastructure;

understand user behavior; and

track key business metrics.

Companies across all industries are re-platforming their businesses to cloud native or hybrid on-premise and cloud infrastructures to enable the digital transformation with software applications. Historically, engineering teams have been siloed, making the development of next generation applications in dynamic cloud environments challenging.

Datadog was founded to facilitate collaboration among development and operations teams, enabling the adoption of DevOps practices. Since then, the company has continuously pushed to unify separate tools, building a real-time data integration platform to turn chaos of having uncorrelated data from disparate sources into digestible and actionable insights. The two slides below illustrate Datadog’s product expansion and innovation over time:

Datadog generates revenue from the sale of monthly or annual subscriptions to customers. The company employs a land-and-expand business model which enables customers to expand their footprint on a self-service basis. Datadog’s customers can enter into a subscription for a committed contractual amount of usage that is apportioned on a monthly basis, a subscription for a committed contract amount of usage that is delivered as used (i.e., billed based on actual usage until they reached the committed amount), or a monthly subscription based on usage.

Usage is measured primarily by the number of hosts or by the volume of data indexed. A host is generally defined as a server, either in the cloud or on-premise. Infrastructure monitoring, application performance monitoring and network performance monitoring products are priced per host, while logs products are priced primarily per log event indexed and secondarily by events ingested.

2. Financial Highlights

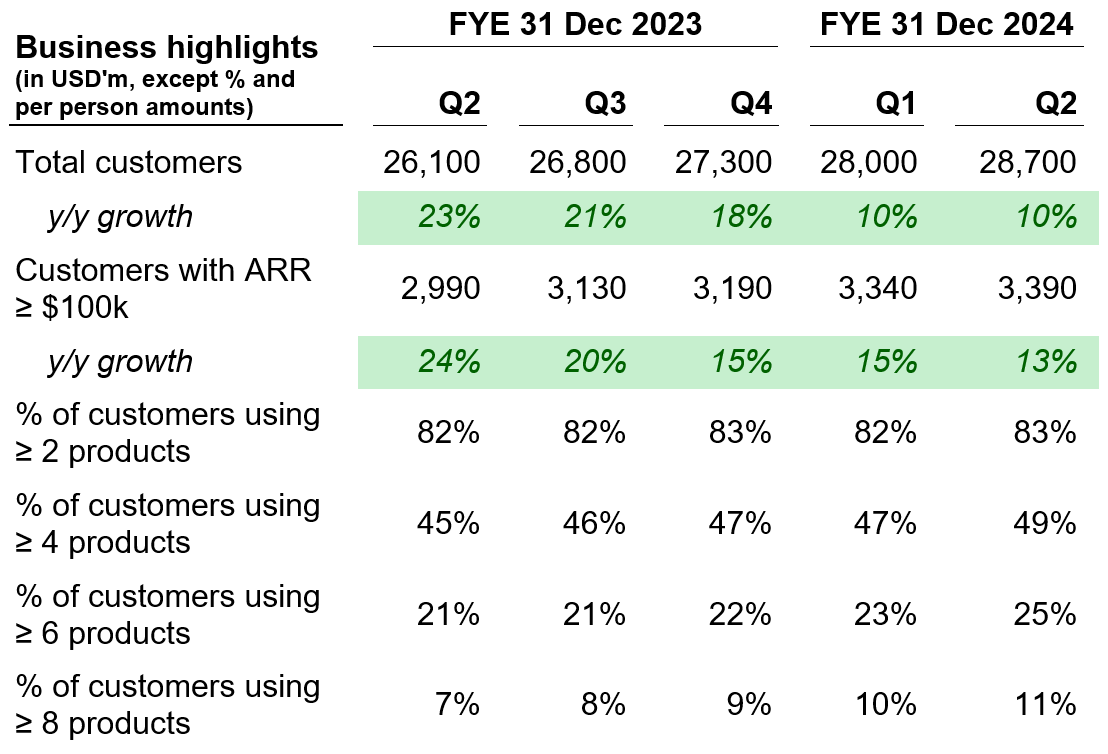

3. Business Highlights

Customer growth

Total Customer Growth

In Q2, Datadog reached 28,700 customers, up 10% from about 26,100 a year ago.

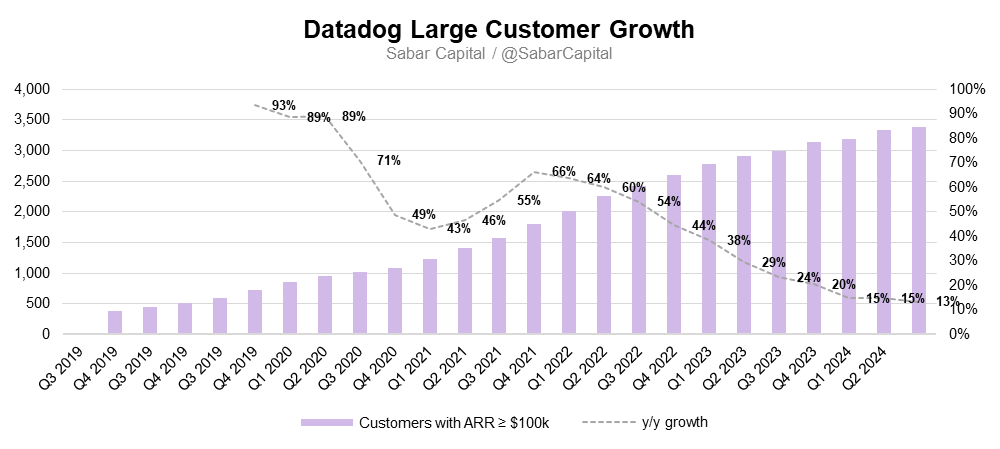

Large Customer Growth

Datadog's large customer base — defined as those with an Annual Run-Rate Revenue (“ARR”) of $100,000 or more — reached 3,390 at the end of the period, representing a 13% y/y increase. These large customers generated about 87% of the company’s ARR.

Note: ARR is defined as the annual run-rate revenue of subscription agreements from all customers at a point in time

Expanding within the existing customer base (Land and expand model)

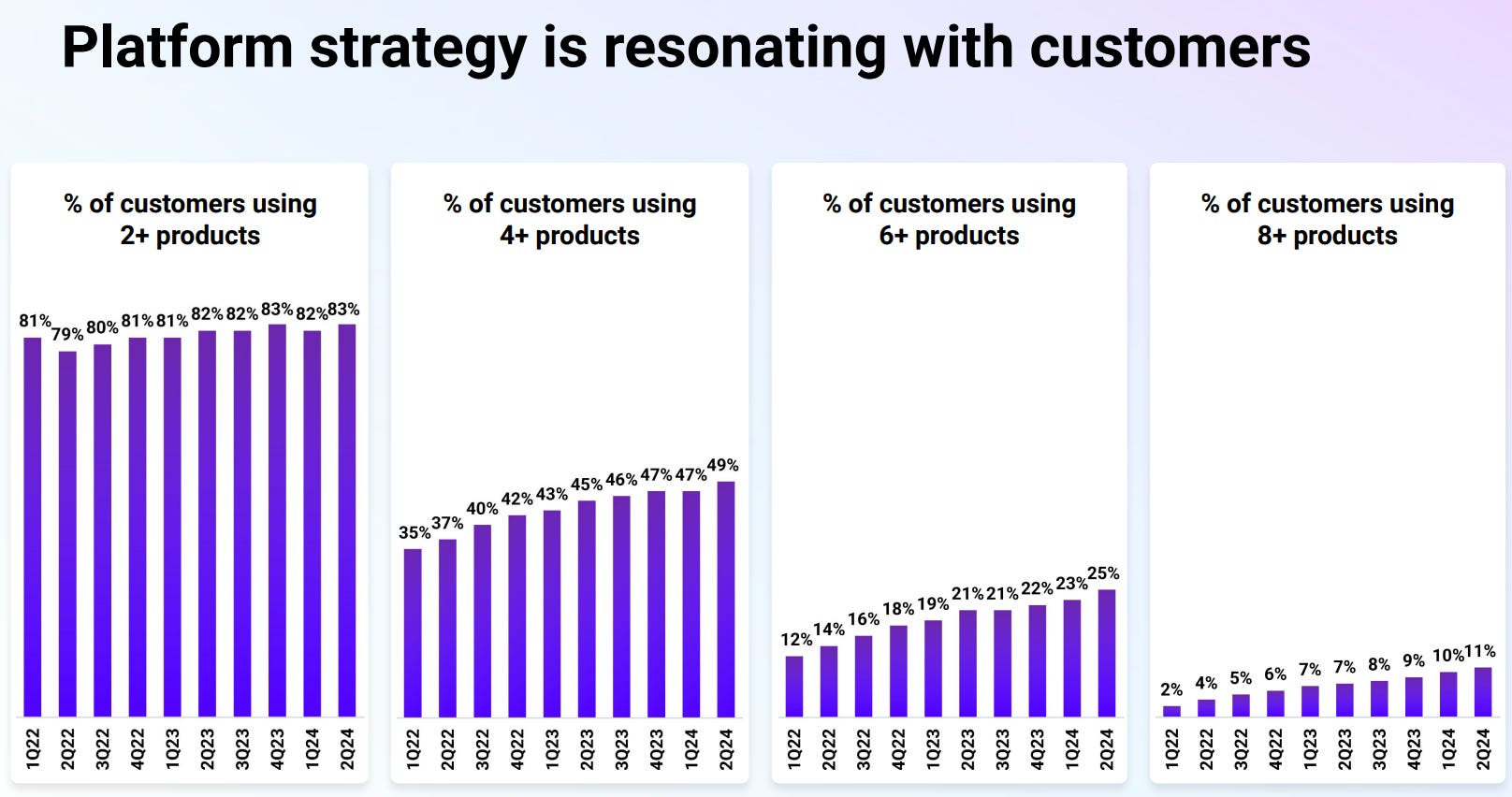

Platform adoption

Datadog’s platform adoption strategy is trending positively. At the end of Q2:

83% of customers were using two or more products, up from 82% a year ago

49% of customers were using four or more products, up from 45% a year ago

25% of customers were using six or more products, up from 21% a year ago

11% of customers were using eight or more products, up from 7% a year ago

Dollar-based Net Retention Rate and Dollar-based Gross Retention Rate

A key metric to measure the propensity of Datadog’s customer relationships to expand over time is the dollar-based net retention rate (“DBNRR”), which compares our ARR from the same set of customers in one period, relative to the year-ago period. In other words, the DBNRR shows how well Datadog is retaining and expanding its business with the same set of customers. For example, a DBNRR above 100% means that Datadog is not only retaining its existing customers but also getting revenue expansion, which can come from increasing customer usage, or upselling additional products.

In Q2, the DBNRR was in the mid-110%s, similar to the past quarters. As recent as 2022, the DBNRR was in the mid-140%s. The decline in DBNRR was mainly due to slower usage growth from existing customers, which could be due to the uncertain macroenvironment. However, management stated that they’ve seen an increasing trend in recent quarters.

On the other hand, the dollar-based gross retention rate (“DBGRR”) measures the company’s retention rate excluding revenue growth from upselling or cross-selling additional products. In other words, it focuses mainly on the retention of the existing revenue base. Datadog’s DBGRR remained stable at the mid- to high 90%s.

Remaining Performance Obligations

Remaining performance obligations (“RPO”) are the aggregate amount of contracts allocated to performance obligations that are not delivered, or partially undelivered at a point in time. They include deferred revenue, multi-year contracts with future installment payments and certain unfulfilled orders against accepted customer contracts at a given period.

While management believes that revenue is a better indicator of business trends rather than billings and RPOs as those can fluctuate on a quarterly basis based on the timing of invoicing and the duration of customer contracts, RPOs can still be a useful indicator for future revenue. Growing RPOs could indicate business stability and be a proxy for customer satisfaction. Further, longer contract duration could be a positive sign of confidence in the company.

In Q2, Datadog’s RPO reached $1.79 billion, up 43% y/y, with contract duration generally increasing as customers choose more multiyear deals. Contract duration increased modestly compared to a year ago.

Billings reached $667 million, up 28% y/y, with billings duration roughly flat compared to the same period a year ago.

4. Financial Analysis

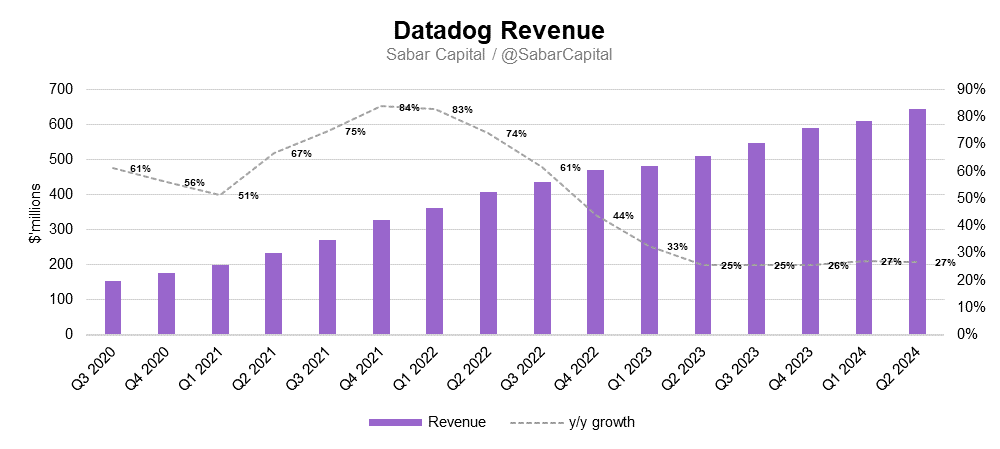

Revenue

Datadog delivered revenue of $645 million, representing a 27% y/y increase. Three thirds of the increase in revenue was driven by growth from existing customers, and the remaining quarter of the increase in revenue was attributable to growth from new customers.

Management stated that usage growth from existing customers was higher than usage growth in the year ago quarter. In the first half of 2024, usage growth was higher than in the first half of 2023. There was strong performance among Datadog’s largest customers as they continue to return to growth and strike a balance between new deployment and focus on optimization. The strongest growth was coming from the enterprise customers which accelerated over the past few quarters, while growth has been more stable for SMB and mid-market customers.

For context, enterprise customers have 5,000 employees or more, mid-market customers have 1,000 to 5,000 employees, and SMB have less than 1,000 employees.

Profitability Analysis

Gross margin increased to 81%, up from 80% a year ago, as revenue growth exceeded the growth of third-party cloud infrastructure provider costs due to cost savings.

Datadog reached an operating income of $12.6 million in Q2, up 157% y/y.

Operating expenses increased by $79.5 million to $509.2 million, up 18% y/y, primarily due to research and development and sales and marketing.

Research and development expense increased by $35.1 million, or 15% y/y due to an increase in personnel costs including allocated overhead costs for engineering, product and design teams as a result of headcount increase.

Sales and marketing expense increased by $39.6 million, or 27% y/y primarily due to an increase in headcount and advertising, marketing and promotional activities.

As a result of revenue increasing by $135.8 million, GAAP operating margin improved significantly to 2%, up from -4.3% a year ago. GAAP profitability has been maintained in recent quarters.

Cash Flow Analysis

Datadog reached a free cash flow of $160 million, up 6% y/y. The chart above shows Datadog’s improving free cash flow over time. Although far from a mature software company, its free cash flow margin is already at 25%. It is important to note though, that stock-based compensation was $135 million in Q2, which we’ll be keeping an eye on. Further, Datadog has net cash position of about $2 billion.

5. Earnings Call Highlights

AI-native customers are ramping up

Today, about 2,500 customers use one or more of our AI integrations to get visibility into their increasing use of AI. We also continue to grow our business with AI-native customers, which increased to over 4% of our ARR in June. We see this as a sign of the continuing expansion of this ecosystem and of the value of using Datadog to monitor the product environment. I will note that over time, we think this metric will become less relevant as AI usage and production broadens beyond this group of customers.

M&A strategy is expected to be more on small and medium-sized deals, and less on bigger deals

Because we have this platform strategy where we're building a consolidator, and we're bringing together many different use cases into one shared platform, we have very broad interest and a very ambitious road map in many different directions. So as a result, we cast a very wide net when it comes to M&A. There's many possible potential fits for us.

So historically, we've been very successful with doing a lot of small and medium-sized deals. At any point in time, we're going to look at a lot of deals that might be small or big. We expect the bigger deal to be fewer and far between, and the bar is very high for those. And today, we're also not looking into anything that would be very material to the business.

The best proxy for future demand in inference spending is the growth of the model providers and AI natives

I would say the best proxy you can get from the future demand there is the growth of the model providers and the AI natives because they tend to be the ones that currently are being used to provide AI functionality into other applications and largely in production environment. And so I always said they are the harbinger of what's to come.

Usage growth is trending upwards, with optimization mostly over, peaking around mid-2023

So when you look at the time series, the peak of the optimization was in Q2, Q3 last year, and we've had a time series of higher usage growth for our clients month-to-month since then. And that's continued through the first half of the year and into July.

Usage growth in enterprises is higher while SMB and mid-market has been more stable

…It's -- the usage growth, as we talked about, is stronger in the enterprise and in the larger users, but it has been fairly stable in the SMB. So we're seeing some more, when you look at the chart in the line, enterprise being -- usage growth being higher than it had been and SMB being stable….

… And for us, I would add that the digital natives are largely SMB and mid-market, they're not enterprise. And even when you look at the digital native, there's two stories, depending on whether you talk about the AI natives or the others. The AI natives are inflecting in a way that the others are not at this point. So today, we see this higher growth from AI natives and from traditional enterprises. And stable growth, but not accelerating, from the rest of the pack….

… Yes. I don't know that there's that much of a trend just yet to look at or there's too much to say at this point. This is just the way the numbers came up in the -- over the past quarter or so.

I would say, look, there's many reasons why the SMBs could be more careful in terms of the macro environment, the fact that there are less -- maybe less -- there's less runway -- immediate runway with consolidation, like things like that, compared to the larger enterprises. And some of them maybe are further along also in their cloud journey, so the growth there is more tied to their overall growth as opposed to their state of transition into next-gen AI and cloud environment. So these are all potential factors….

LLM observability has to be integrated with the rest of the stack because LLM doesn’t work in a vacuum

Yes, I think, so the first thing I'd say is we expect this market to change a lot over time because it is far from being mature. And so a lot of the things that might happen today in a certain way might happen 2 years in a very, very different form.

That being said, the way it works typically is customers build applications using developer tools, and there's a whole industry that has emerged around developer tools for -- and playgrounds and things like that for LLM. And so they use not one, but 100 different things to do that, which is fairly similar to what you might find on the IDE side or code editor side for the more traditional development, which is lots of different, very fragmented environment on that side.

When they start connecting the LLM to the rest of the application, then they start to need like visibility that includes the other components because the LLM doesn't work in a vacuum, it's plugged into a front end. It works with authentication and security. It works with -- connects to other system databases in other services to get the data. And at that point, they need it to be integrated with the rest of the observability.

For the customers that use our LLM Observability product, they use us for the rest -- all the rest of their stack. And it would make absolutely no sense for them to operate their LLM in isolation completely separately and not have the visibility across the whole applications. So it's -- at that point, it's a no-brainer that they need everything to be integrated in production.

Gross margins may fluctuate from quarter to quarter as new products are launched and optimized

…But essentially, what we said consistently is that gross margins have operated in a range, they've operated towards the top of the range. But there will be variability quarter-to-quarter as we launch functionality, often having to do with rolling out functionality and then optimizing it. And so the movement -- slight movements that we've seen quarter-to-quarter have been the result of that….

…Yes. There's definitely nothing to read into the small movements in the gross margin from a product mix perspective. A lot of what happened is we build new features, maybe some of you saw these new features, will have more compute impact and more storage impact or something else. Maybe also they won't be fantastically optimized on day one from an, I'll call, efficiency perspective. Or maybe sometimes, we'll focus more on building more things as opposed to optimizing them because they are the same people, same resources on our end that work on both. And so what you should expect to see some ebbs and flows on that number as we keep shipping new feature and then we keep optimizing.

In general, we feel good about the gross margins. We're not constrained in terms of what we can build by the margin profile we have. And also, should we need them, we have many levers to improve these margins as well. So we wouldn't read too much into the small changes. I would expect some of those small changes in the future. And in all, we feel good about that….

Three-thirds of growth is from existing customers as opposed to new customers

It's going to be 75-25. 25% from new, 75%, which would be what we said all along is that, as net retention recovers and usage growth is higher than the previous comparable period. As -- if you go back through our history, you will see that the amount from existing customers relative to new logos has generally increased.

6. Takeaway

Strong quarter from Datadog with continued customer growth and effective product upselling strategy with net retention rate above 110%. Although revenue growth has slowed down relative to 2020-2022, it’s still fairly strong at 27% y/y. Since the optimization for cloud spending seems to have peaked in mid- to late 2023, Datadog’s revenue growth could begin re-accelerating as cloud spending picks up.

Datadog has managed their costs and returned to GAAP profitability in recent quarters, while maintaining strong free cash flow. Overall, strong performance from the company with a large and growing TAM that is still in its early innings.

Disclaimer: Please note that none of the information provided constitutes financial, investment, or other professional advice. It is only intended for educational purposes. We have a vested interest in Datadog Inc. Holdings are subject to change at any time.

Great analysis!