The Trade Desk: A Growth Story That Keeps Compounding

The Trade Desk (“TTD”) Q2 2024 Earnings Analysis

1. About TTD

The Trade Desk is a self-service, omnichannel cloud-based software platform that enables advertisement buyers to create, manage, and optimize more expressive data-driven digital advertising campaigns across ad formats, including display, video, audio, native and social, on a multitude of devices, such as computers, mobile devices, and connected TV (“CTV”).

The company serves advertising agencies and other service providers for advertisers. The company mainly generates revenue by charging clients a platform fee based on a percentage of the client’s total spend on advertising.

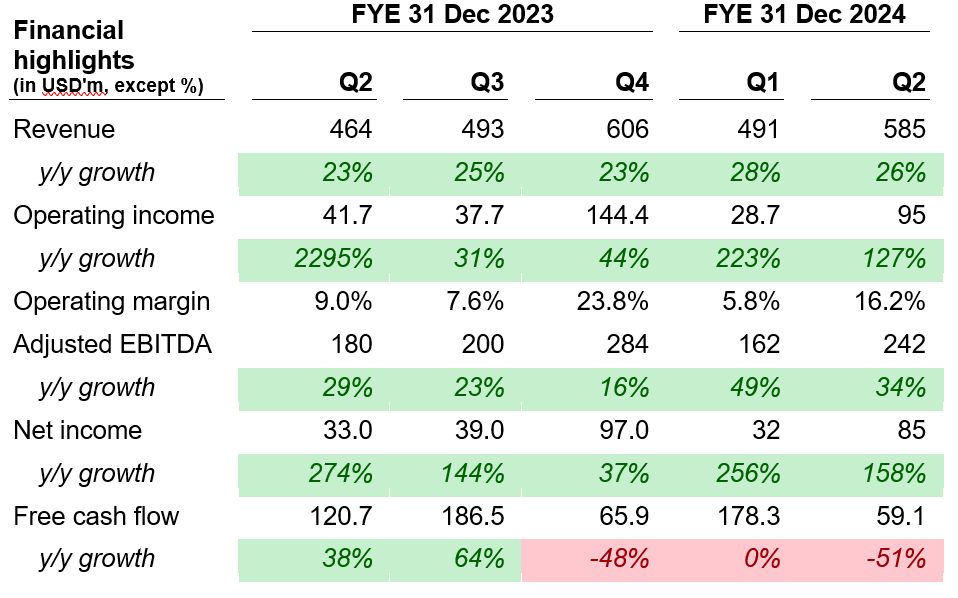

2. Financial Highlights

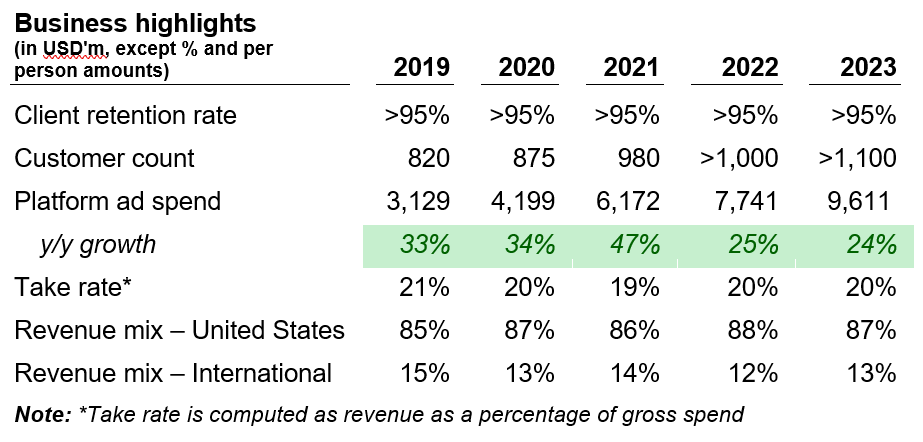

3. Business Highlights

Of the above, the only two metrics that are disclosed quarterly are the client retention rate and the geographical revenue mix. The rest of the metrics in the above table are only disclosed on an annual basis.

Client Retention

The client retention rate this quarter was more than 95%, which was the case for the past 10 years consecutively.

Geographical Revenue Mix

The revenue mix remains somewhat stable with 88% in the US and 12% in international. As management claimed that about two thirds of the total addressable market is outside of North America, the revenue mix should trend towards international over time.

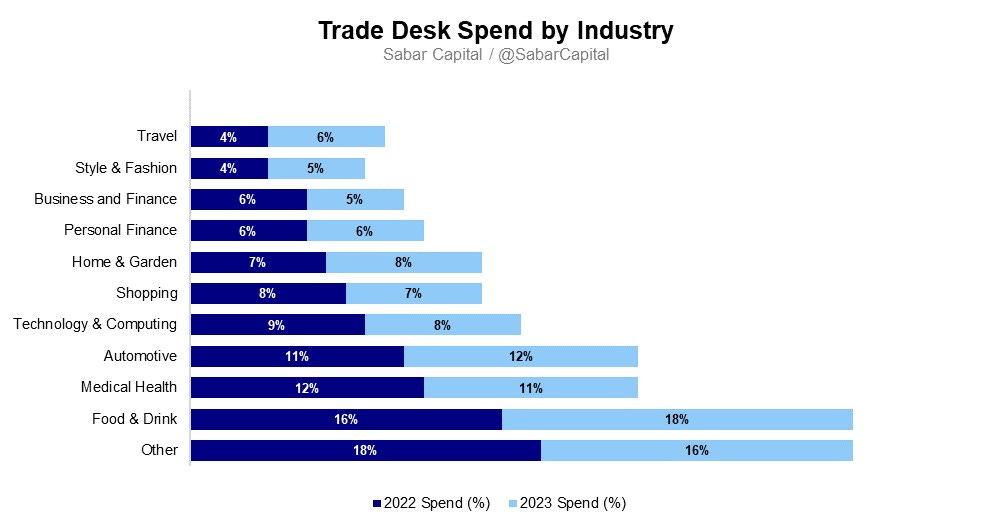

Gross Spend by Industry

The Trade Desk’s gross spend continues to be well-diversified across major verticals as shown in the chart below.

Updates on CTV:

The Trade Desk to be one of Netflix’s main programmatic partners for advertisers, as part of Netflix’s effort to expand their buying capabilities

FOX announced an expanded partnership with The Trade Desk through integration of UID21 and OpenPath2 across FOX brands and the AdRise technology platform

E.W. Scripps is streamlining its programmatic ad buying process for advertisers through the adoption of OpenPass3 and UID2, making it the first CTV publisher to adopt OpenPass; and

At Forward ‘24 in Canada, CBC announced its Olympics inventory will be available programmatically for the first time ever via The Trade Desk.

Updates on UID2:

Roku announced its adoption of UID2, allowing advertisers to implement more precise targeting and a secure means to facilitate data collaboration with Roku Media;

SiriusXM Media announced Pandora Media as the first audio publisher to adopt UID2;

LG Ad Solutions announced it is integrating UID2 to enable advertisers to leverage their first-party data across LG’s extensive audience network in a privacy-conscious manner; and

TF1, M6, and Media Figaro, three of the leading broadcasters and publishers in France, announced their adoption of EUID to help their advertisers run effective campaigns with improved targeting capabilities.

4. Financial Analysis

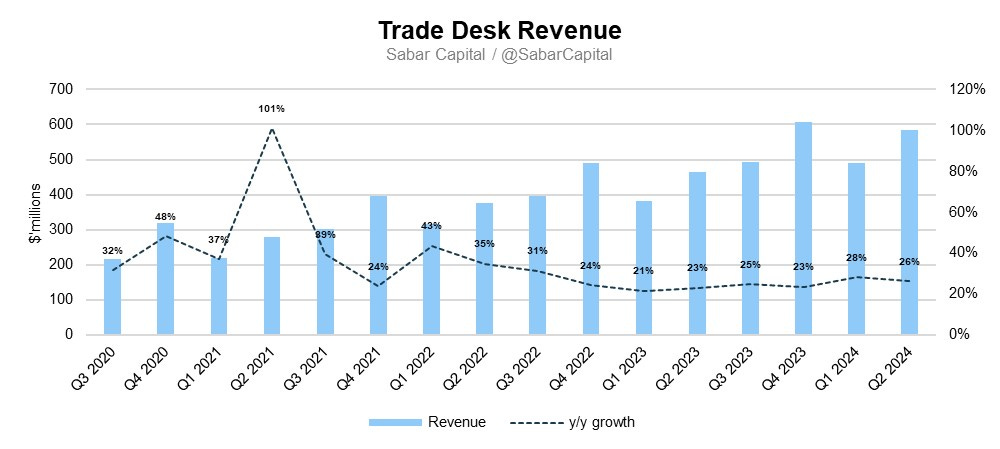

Revenue

The Trade Desk delivered revenue of $585 million, representing a 26% year-over-year increase. This growth was mainly driven by higher gross spend in the current year on the platform, which in turn was driven by new clients and more campaigns executed by existing clients.

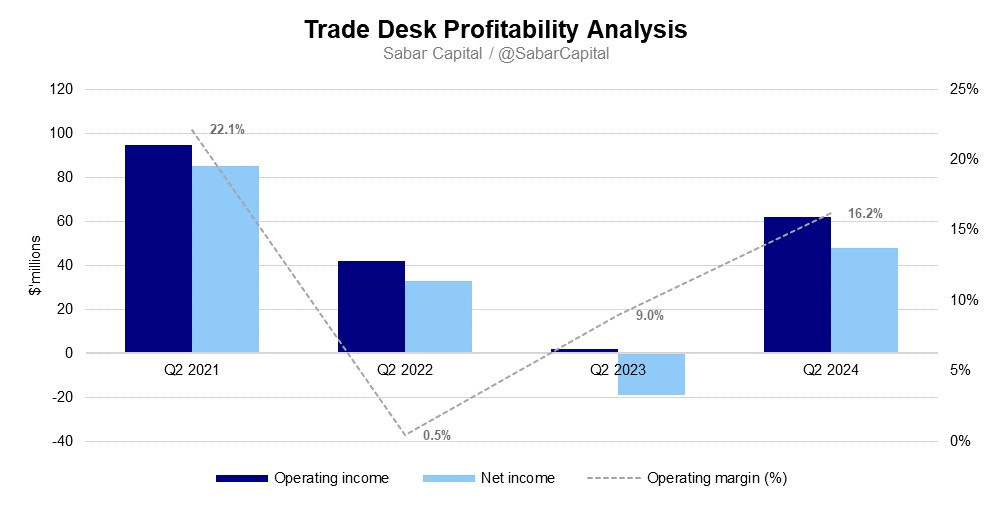

Profitability Analysis

In Q2 2024, The Trade Desk reached an operating income of $95 million, up 127% y/y.

Operating expenses increased by $67 million to $489.8 million, up 16% y/y, mainly due to platform operations expense and sales and marketing.

Platform operations expense increased by $24 million, or 27% y/y driven by an increase in hosting costs due to support costs related to:

the increased use of the platform by clients;

increased use of features by the company’s technical teams in platform support; and

investment in new data centers to support the continued platform growth.

Sales and Marketing expense increased by $22 million, or 20% y/y due primarily due to an increase in personnel costs as the company increases headcount growth in support of their sales efforts.

As a result of revenue increasing by $120 million, almost double compared to operating expenses of $67 million, operating margin improved significantly to 16.2%, up from 9% a year ago.

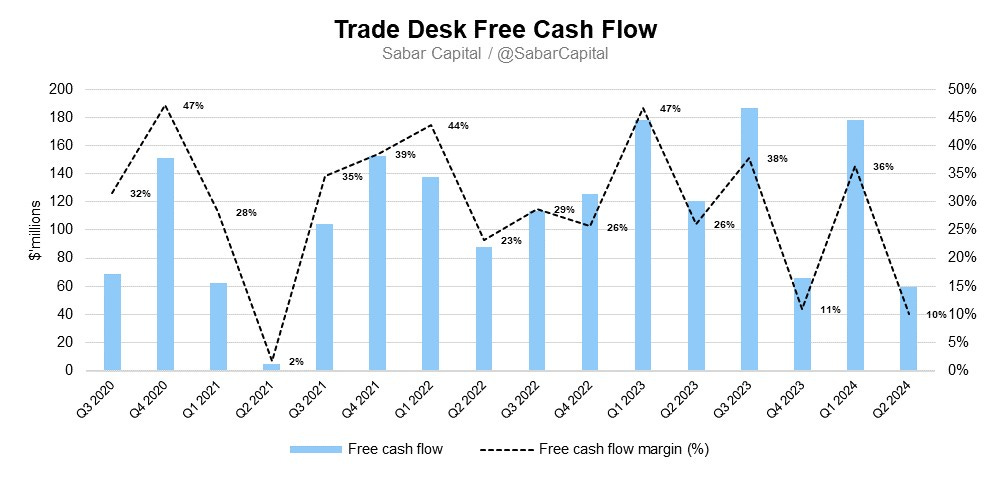

Cash Flow Analysis

Overall, free cash flow for The Trade Desk is strong, with the trailing last 12 months (LTM) free cash flow margin at 22.5%. The company has $1.5 billion of cash and cash equivalents on the balance sheet, with no debt.

5. Earnings Call Highlights

Companies are being pressured for higher return on investments with less ad spend

…Nonetheless, CMOs are being asked from CFOs to deliver growth. CFOs are saying, we have to have real growth now, and that puts more pressure on the CMOs than ever. And of course, they're in an environment with inflation and some consumer weakness and some higher interest rates and a bunch of other macro themes that investors know all too well.

But those pressures are actually creating a better macro environment for us. All of those things, including some of the pressures on the sell side, create a buyer's market. And the pressures on CMOs create data-driven, rational buying. And they're looking to us to help them put their data to work and make more informed decisions. They're being asked to do more with less. They're being asked by their CFO to prove that the ROI is better. It's no wonder they're coming to us asking for joint business plans and saying, how can we build long into the future, especially when there seems to be no other company in the world more focused on the open Internet and helping to monetize that for all the great premium content owners on the open Internet, but of course, representing the buyer to help them figure out what is best for them…

…One top CMO talks about the difficulty of what he described as "the illusion of growth" where it appears that companies are doing well, stock prices are up, but the average consumer feels more constrained than ever in terms of purchasing power. That has significant implications on how companies market products from pricing to packaging to advertising. And perhaps more than anything else, it's putting a premium on the efficacy of marketing.

More than ever, CMOs have to prove that what they are doing is working. And increasingly, that means revising traditional dependencies on cheap reach and all the legacy mechanisms and beliefs that support cheap reach. It means embracing the power of programmatic data-driven advertising. We are convinced that the only scaled response to all the changes CMOs and the agencies are facing is to embrace data-driven buying…

There’s a disconnect between Big Tech Walled Gardens (i.e., Facebook, Instagram, YouTube)’s cheap reach and longer-term business results

For many marketers dealing with macro uncertainty over the last few years, this cheap reach solution has been attractive. But more and more CMOs, especially those at the world's leading brands, have become concerned with the flaws in this strategy for a number of reasons. A few of those. First, much of the mass scale is predicated on cheap, owned and operated content, which is often just user-generated videos or social content that is essentially free to produce and ultimately, mostly lower quality and higher risk for large advertisers.

The big tech owners of this content have an inherent incentive to direct demand toward it because the margins on it are so significant. But it's often not where the marketers target customers spend most of their time nor where they're the most leaned in.

Second, after several years of uncertainty, the business flaws of cheap reach are more apparent than ever. If a CMO has been going to the CEO or CFO and saying, look, I was able to drive down costs, and the scorecard says it's working. But then a couple of years later down the road, business results are not consistent with those marketing metrics. And as a result, there's a disconnect. This is arguably one of the main reasons that CMOs have the shortest tenure on the C-suite. Marketing performance data predicated on cheap reach that doesn't match up with the business outcomes over time.

Consumers are shifting to the Open Internet i.e., CTV and digital audio…

…One of the trends that, that report showcases is the massive shift over the last 4 years in terms of where consumers are spending their digital time. It used to be that consumers spend about 60% of their time within walled gardens and 40% on the open Internet. That trend has completely reversed since the pandemic. Why? Well, in large part, it's because of the mass consumer shift to emerging premium open Internet channels such as CTV and digital audio.

In the U.S., over the last decade or so, consumers have doubled the time they spend in these 2 channels alone to around 5 hours per day, significantly more than they spend on social media…

…On average, in the U.S., consumers spend around 3 hours per day listening to music, podcasts and other types of digital audio. And yet digital audio commands a small fraction, by comparison, of advertising demand. But that's beginning to change, especially as companies like Spotify make investments to enable more programmatic and automated buying, as they highlighted in their most recent earnings call…

…and engagement on CTV and digital audio is much higher quality

Companies like Spotify, Netflix, Disney, Warner Bros., Discovery and others have fundamentally changed the way that consumers behave. I would also add that the time that consumers spend in these channels is much more leaned in and engaged than the time spent on channels such as social media. You're much more leaned in when watching the latest hit show or the Olympics or listening to your favorite podcast than you are watching endless short videos of teenagers pulling wheelies on the West Side Highway.

CTV was the leader in growth, followed by mobile, display and audio

From a scale channel perspective, CTV, by a wide margin, led our growth again during the quarter. In Q2, video, which includes CTV, represented a high 40s percentage share of our business and continues to grow as a percentage of our mix. Mobile represented a mid-30s percentage share of spend during the quarter. Display continued to represent a low double-digit percent share of our business, and audio represented around 5%.

Broad-based growth in ad spend across verticals

We saw strong performance in the majority of our verticals, particularly in home and garden, food and drink, and shopping. Family relationships and healthy living verticals were both below average. Overall, we continue to see healthy trends across our verticals, and we continue to believe there is opportunity for us to gain share in the verticals we serve.

The walled garden playbook doesn’t work in CTV because the CTV market is fragmented

…I would argue that the decisions that they made are to join the open Internet and to recognize that the walled garden playbook doesn't really work in CTV.

And the reason why the walled garden playbook doesn't work in CTV is because nobody has enough share to be draconian or even to target well, even to be effective, because of the fact that TV is fragmented. There is no one single player that has anything close to what Facebook does in social or what Google has in search.

So as a result, if you house a bunch of inventory there and then don't enable people to bring data to work from other places, it will not perform as well. And so it is true that more inventory has been coming online in CTV, but what is -- what sometimes I think is lost, especially in discussions about CPMs, is that there is a greater desire for marketers to find their exact audiences than they've ever been or there has ever been.

Amazon’s conflict of interest with ad buyers

And they're look -- they have to look across all these different pools of inventory in order to find the small pieces in each of them that give them the efficacy that they need to be effective and to put their dollars to work as effectively as possible. That's only possible when you're looking across the entire open Internet. And when you consider the fact that perhaps our greatest strategic asset is that we are objective, that we don't own media, and so as a result, we can help the biggest brands in the world objectively figure out whether they should buy Hulu or Netflix or Spotify or Yahoo.

And that objectivity is in greater compromise, I would argue, at Amazon than anywhere. And that's in large part because not only does Amazon have its own owned and operated inventory as it relates to CTV inventory. It also operates as the second-largest search engine in the English-speaking world, and then it also competes in building products with almost every major advertiser in the world.

Note: Amazon has both an ad inventory and a Sell-Side Platform (“SSP”). The SSP sells both Amazon’s and other advertisers’ inventory, which means Amazon and other advertisers compete for inventory. Given that Amazon has a data advantage through its Bing search engine, and the fact that it competes with other advertisers in building products (Amazon’s private label products), it can easily use the information in their favor when it comes to ad inventory decisions.Along with CTV, retail media is a threat to walled gardens due to the accuracy of measurement in ads

And I've mentioned before that I believe the 2 greatest threats to walled gardens and the bringing down of their walls are: number one, CTV for all the reasons we've talked about on this call; and number 2, retail media.

And the retail media is important because it changes the measurement game. So a few times in the prepared remarks and in the comments, I've mentioned some of the flaws of measurement inside of walled gardens. But if you're actually connecting the ads that you show to a specific user and then the purchase that they make later, it becomes much more irrefutable to show the connection between the ad shown and the purchase. And retail just has tremendous promise for that.

And not only is that good for advertisers, but that is also good for retailers who are all trying to find their way to compete in the digital world and to compete with the Amazons of the world. So our partnerships with companies like Walgreens and Walmart and Target and so many others are just great examples of the opportunities that exist in retail media, and we have merely scratched the surface

Publishers absolutely need to have an identity and authentication strategy

And for publishers, they need to have an identity strategy and an authentication strategy. And what I mean by that is when it comes to authentication, if you're not in CTV or audio where 100% of your users log in, and that's not true of all CTV players but that's true of most of them, then you need to find a way to get them to log in and to address consent. In other words, ask them if you can provide them with personal content and create a quid pro quo that makes it worth it.

Everybody needs to be developing that strategy, especially if you're in browser right now. So they've been given a bit more time, but they need to use that time to act. And even if Google does nothing more, you have to use that time to act simply because things like UID are so effective for CTV and audio and other channels and for those that have log-ins even in the browsing world, that it will make it so that we prioritize that media over those that are just dependent on cookies or something else. So naturally, over time, it becomes very important.

And this is more important for those in journalism than anywhere. Just because they tend to move very slow and not be technological innovators, so it becomes really important that they respond to that. And advertisers, if you're not putting your data to work with an identity strategy, in other words, how can I use my data in a consumer-friendly way and pricing-centric way, how can I put my data to work so that I can do better marketing?

If you're not thinking about that and honoring the sort of sacred relationship that you have with your customers, then you're doing it wrong and you're likely to lose to those that are doing that. So there's a fair amount of pressure on both buy side and sell side to sort of get with the times. And all of this change is happening so fast, but all of that has created an opportunity for us at an unprecedented pace. And that's part of the reason why we're so bullish.

6. Takeaway

The Trade Desk’s results this quarter were strong overall, with robust revenue growth, strong free cash flow and a solid net cash balance sheet. The growth in advertising spend is broad-based across well-diversified business verticals. The company’s client retention rate has been maintained at above 95% for the past 10 years, which speaks volumes to the quality of the service they provide.

Additionally, there’s a long runway for growth ahead for the company. CTV is the largest and fastest growing channel; both Netflix’s ad-supported plan rollout and Amazon Prime setting the ads-supported plan as default are making it increasingly clear that being ad-funded is the way forward. Digital audio remains an emerging channel for ad spend. Despite US consumers spending around 3 hours a day listening to digital audio, it currently captures only a small share of advertising dollars.

The retail media opportunity is another growth driver, which enables deterministic insights and verifiable information about consumers. By plugging in or activating shopper data with closed-loop attribution, marketers can now measure, optimize (in midflight) and attribute ad campaigns to business outcomes. Moreover, there is significant room for international growth. While the majority of The Trade Desk's revenue comes from the U.S., two-thirds of global advertising dollars are spent outside North America

Overall, this is a company with strong fundamentals that seems well-positioned for long-term growth.

Disclaimer: Please note that none of the information provided constitutes financial, investment, or other professional advice. It is only intended for educational purposes. We have a vested interest in The Trade Desk Inc. Holdings are subject to change at any time.

Unified ID 2.0 (“UID2”) is an open-source framework that publishers, advertisers, and digital advertising platforms can use to establish identity without third-party cookies. To read more about UID2, click here.

OpenPath provides The Trade Desk clients with a simplified, direct connection to participating premium publishers across the open internet, allowing advertisers to access premium publisher content directly on the The Trade Desk’s platform. To read more about OpenPath, click here.

OpenPass is a streamlined single sign-on (SSO) solution that helps consumers view content in exchange for personalized advertising. With this solution, consumers can access premium content across the open internet using just their email addresses.